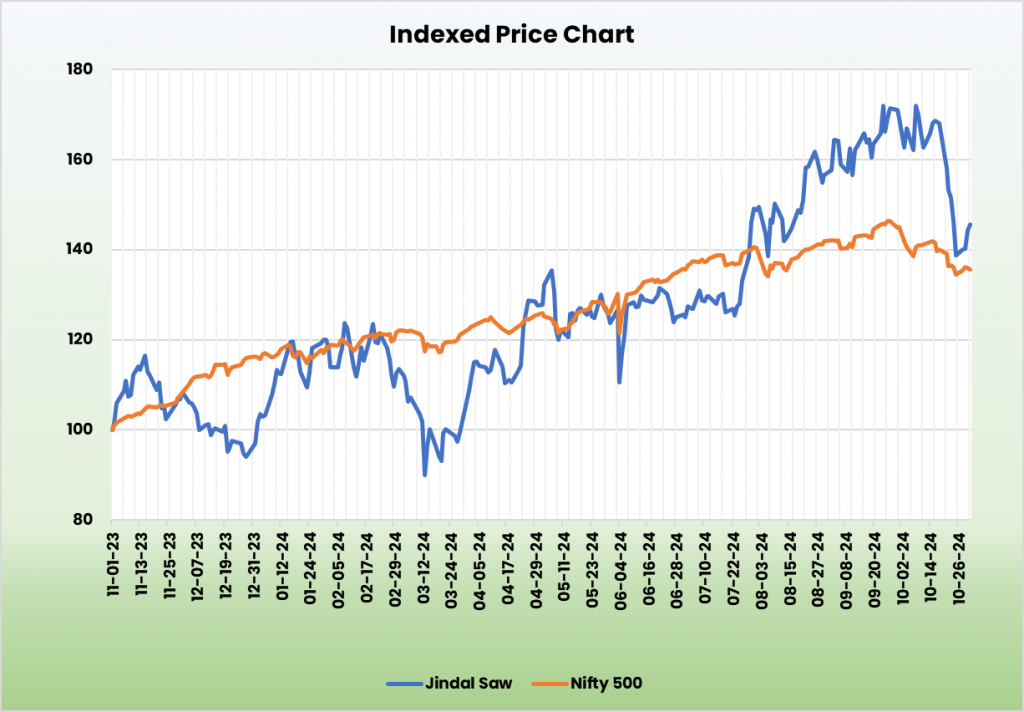

Jindal Noticed Ltd – Whole Pipe Options

Based in 1984, Jindal Noticed Ltd. has established itself as a market chief within the pipe manufacturing trade, supplying important infrastructure supplies for sectors like oil & fuel, water, and industrial engineering. With operations throughout India, the USA, Europe, and the UAE, the corporate offers an in depth portfolio starting from SAW pipes for vitality transportation to ductile iron pipes for water administration, catering to a world shopper base of main oil corporations and engineering companies.

Merchandise and Providers

- SAW Pipes – Used primarily for oil, fuel, and water transportation.

- Ductile Iron & Carbon Alloy Pipes – Serving water transportation and numerous industries like automotive, energy, and course of industries.

Subsidiaries: The corporate operates with 8 direct subsidiaries, 13 oblique subsidiaries, 1 affiliate, and 1 three way partnership as of FY24.

Development Methods

- World Market Attain – Jindal Noticed’s sturdy worldwide presence is supported by a strong order guide of $1.65 billion, 32% of which is sourced from international purchasers.

- Give attention to Water & Irrigation – About 70% of present orders are for water and irrigation tasks, reinforcing the corporate’s stronghold on this sector.

- Entry into the U.S. Market – New seamless and stainless merchandise are set to seize U.S. market demand and enhance total margins.

- Infrastructure Investments – The corporate is enhancing its Mundra coke oven battery for elevated electrical energy technology and improved coal throughput, with Rs.300-350 crore allotted for the venture.

- Nashik Plant Growth – Investing Rs.200 crore to diversify manufacturing with new furnaces and bigger pipe diameters, growing capability by 40-50%.

- Capability Debottlenecking at Haresamudram – Expansions are anticipated to raise ductile iron manufacturing to three lakh tonnes, making it one in all India’s prime producers.

- Innovation and Effectivity – Upgrading processes to boost capability and effectivity throughout services, strengthening aggressive benefit available in the market.

Monetary Efficiency

Q2FY25

- Income: Rs.5,572 crore (+2% YoY)

- EBITDA: Rs.914 crore (+14% YoY)

- Internet Revenue: Rs.475 crore (+33% YoY)

FY24

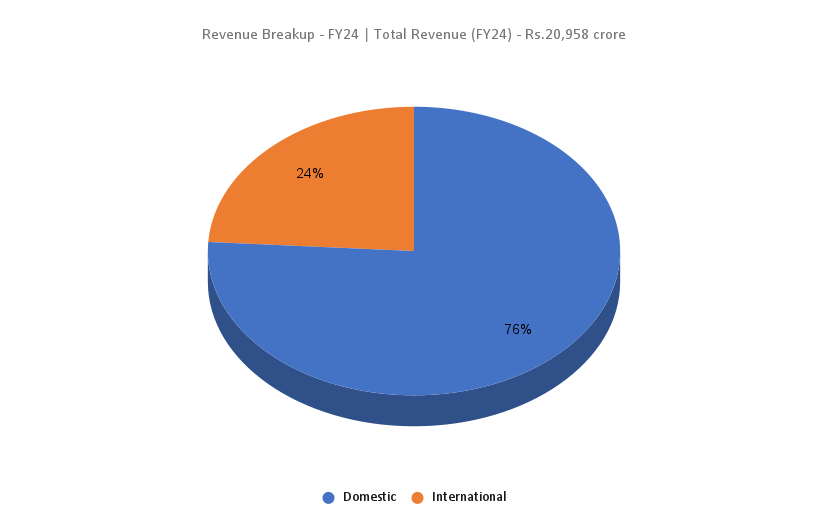

- Income: Rs.20,958 crore (+17% YoY)

- Working Revenue: Rs.3,326 crore (+98% YoY)

- Internet Revenue: Rs.1,593 crore (+252% YoY)

Monetary Efficiency (FY21-24)

- Income and Internet Revenue CAGR: 25% and 71%

- Common ROE & ROCE: 10% and 14%

- Debt-to-Fairness Ratio: 0.51

Business outlook

- Rising Water Demand – India’s improvement requires intensive water infrastructure for each industrial and home wants.

- Authorities Initiatives – Funding in tasks like irrigation, river purification, and the AMRUT-2.0 scheme drives demand for water transmission options.

- Pipeline Growth – Plans to extend pipeline protection by 54% to 34,500 km by 2024-25.

- Vitality Demand Surge – Financial progress is fueling the necessity for improved vitality transport infrastructure.

- Wastewater Infrastructure – Rising sewage technology at a 4.7% CAGR underscores the necessity for superior wastewater methods.

Development Drivers

- FDI Incentives – 100% FDI permitted in oil, fuel, and associated infrastructure.

- Pipeline-based Irrigation – Adoption in numerous states, supporting water conservation.

- City Water Schemes – Initiatives like AMRUT-2.0 and Good Metropolis to spice up demand.

- Infrastructure Investments – Growth in pure fuel and water pipelines.

Aggressive Benefit

Jindal Noticed’s secure income progress and constant returns make it undervalued in comparison with friends like Jai Balaji Industries and Venus Pipes & Tubes.

Outlook

- Robust Order Pipeline – With a $1.6 billion order guide, the corporate’s pipeline contains 70% water and irrigation tasks and 25% oil and fuel, offering a balanced income stream.

- Improved EBITDA Margins – Steerage targets a 19% EBITDA margin as stabilization in metal costs aids profitability.

- New Product Strains – Expanded product choices and entry into new segments place Jindal Noticed for sustained progress.

- Export Development Technique – Aiming to extend export income to 20-25%, up from the present 12%.

- Father or mother Firm Assist – The O.P. Jindal Group’s backing offers monetary and strategic energy to gas additional progress.

- Effectivity and Capability Positive aspects – Debottlenecking and enlargement initiatives throughout vegetation will drive operational efficiencies and manufacturing capability.

- Lengthy-term Development Potential – These strategic strikes underscore Jindal Noticed’s dedication to capturing rising alternatives in infrastructure and industrial segments globally.

Valuation

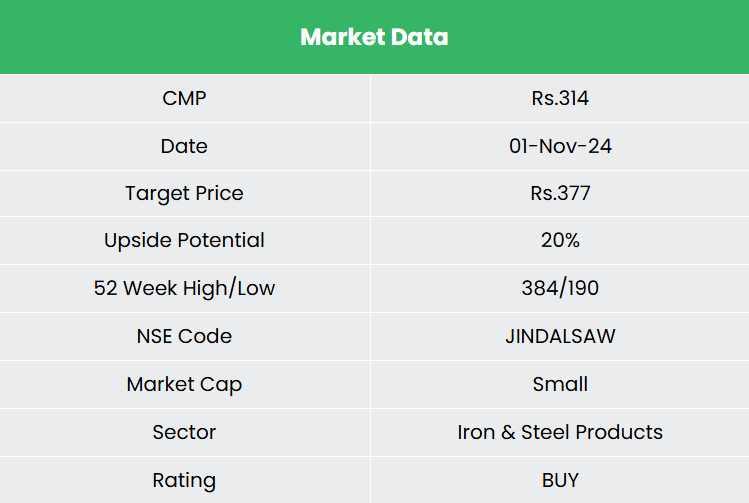

We suggest a BUY with a goal value of Rs.377 (12x FY26E EPS), backed by stable fundamentals and progress initiatives.

Dangers

- Geopolitical Instability – Potential provide chain disruptions affecting operations.

- Market Competitors – New entrants within the DI pipes market might influence market share.

Be aware: Please be aware that this isn’t a suggestion and is meant just for instructional functions. So, kindly seek the advice of your monetary advisor earlier than investing.

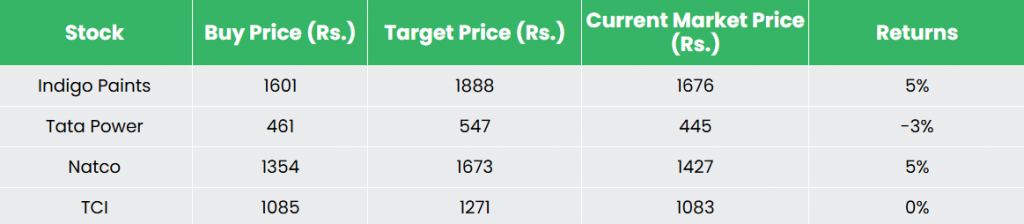

Recap of our earlier suggestions (As on 01 November 2024)

Indigo Paints Ltd

Tata Energy Firm Ltd

Natco Pharma Ltd

Transport Company of India Ltd

Different articles you might like

Put up Views:

114