Indigo Paints Ltd – Vibrant Shades of Outperformance

Indigo Paints Ltd., established in 2000 and primarily based in Pune, is one in all India’s fastest-growing ornamental paint corporations. Initially targeted on economical cement paints, it has since expanded right into a broad vary of ornamental paints and building chemical substances, together with waterproofing by way of a 51% stake in Apple Chemie India Pvt Ltd. Indigo Paints operates 5 manufacturing services throughout Jodhpur, Kochi, and Pudukkottai, with over 18,000 lively sellers, 53 depots, 9,842 tinting machines, and a presence in 28 states as of FY24.

Merchandise and Providers

Indigo Paints presents a variety of merchandise, together with emulsions, enamels, wooden coatings, primers, distempers, cement paints, putties, and specialised options like Aquashield, Crack Heal Paste, Damp Seal, Damp Cease, Poly Restore, and Superseal.

Subsidiaries: As of FY24, Indigo Paints Ltd. has one subsidiary and no associates or joint ventures.

Development Methods

- Product Diversification via Acquisition: Acquired a 51% stake in Apple Chemie, a fast-growing participant in building chemical substances and waterproofing, yielding 24% progress in FY24 and 47% in Q1FY25 YoY.

- Main Undertaking Collaborations: Apple Chemie equipped supplies for vital nationwide initiatives, together with the Mumbai Trans Harbour, Atal Setu, and Versova-Bandra Sea Hyperlink.

- Market Enlargement: Past its authentic Maharashtra focus, Apple Chemie has now established advertising groups throughout Karnataka, Bihar, Telangana, Tamil Nadu, Odisha, West Bengal, Madhya Pradesh, and Delhi NCR.

- NABL Accreditation: First building chemical substances firm in India to attain NABL accreditation for its laboratory.

- Capability Enlargement: New crops in Jodhpur are underneath building, with capacities of 12,000 KLPA/MTPA for solvent-based merchandise, 90,000 KLPA/MTPA for water-based, and 138,000 KLPA/MTPA for powder-based merchandise. A 50,000 KLPA/MTPA water-based facility in Pudukkottai started operations in September 2023.

- Community and Seller Enhancement: Actively growing the seller base and tinting machine installations, which have boosted seller gross sales by 3-4 instances via larger throughput.

Operational Efficiency

Q1FY25

- Income Development: Income rose to ₹311 crore, marking an 8% year-over-year improve.

- Revenue Decline: Decrease realizations, elevated manpower, and depreciation prices from the brand new plant (operational since September 2023) led to a lower in earnings.

- Working Revenue: Fell by 3%, totaling ₹47 crore.

- Web Revenue: Declined by 15% to ₹27 crore.

- Gross sales Pressure Enlargement: Gross sales staff grew by ~40% in Q2FY24, aiming to spice up market attain.

- Market Affect: The subdued demand in Kerala, a key income supply, affected total efficiency for the quarter.

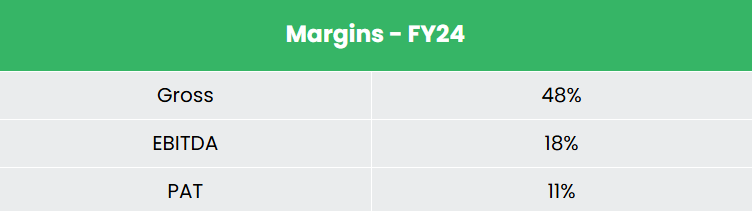

FY24

- Income: ₹1,306 crore, up 22% YoY.

- Working Revenue: ₹238 crore, a 31% YoY improve.

- Web Revenue: ₹149 crore, marking a 28% YoY progress.

Monetary Efficiency (FY21-24)

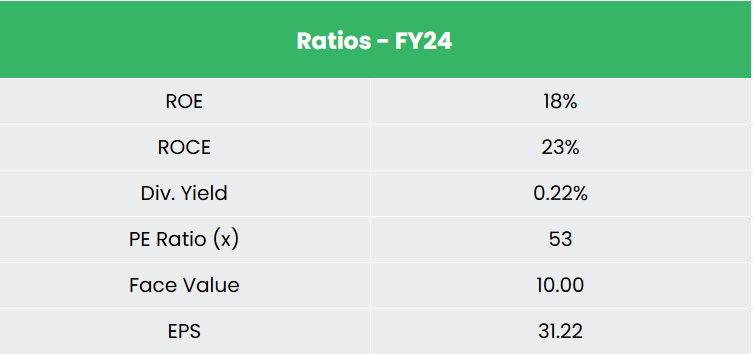

- 3-12 months CAGR: Income grew at 20%, and web revenue at 28% (FY21-24).

- Return Ratios: Common ROE at 17% and ROCE at 21% over FY 21-24.

- Capital Construction: Robust with a low debt-to-equity ratio of 0.02.

Business outlook

- Paints and Coatings Market: Pushed by inhabitants progress and urbanization, India’s paints and coatings market (ornamental and industrial) was valued at USD 13,405.4 million in FY24, projected to achieve USD 31,706.3 million by FY33 with a CAGR of 8.75%.

- Waterproofing Options Market: Anticipated to develop from USD 1.18 billion in 2024 to USD 1.81 billion by 2030, at a CAGR of seven.44%.

- Development Chemical substances Market: Projected attain USD 5.02 billion by 2030, rising at a CAGR of seven.24%.

Development Drivers

- City Improvement Initiatives: Packages just like the Sensible Cities Mission and Housing for All drive building actions, creating demand within the paint and coating trade.

- Development Sector Development: Increasing business and residential building, supported by favorable authorities insurance policies, boosts demand for building chemical substances and waterproofing options.

- Automotive Sector Demand: Development in automotive gross sales and after-sale providers throughout segments is growing the necessity for specialised paints and coatings.

Aggressive Benefit

Indigo Paints is producing constant gross sales progress with steady returns on invested capital and boasts larger revenue margins (18%) in comparison with rivals like Akzo Nobel India Ltd and Kansai Nerolac Paints Ltd, highlighting its robust potential for earnings enlargement.

Outlook

- Class Management: Established as a pacesetter in lots of product classes, facilitating simple entry into Tier 3 and 4 markets, giving them pricing energy and expanded margins.

- New Product Launches: Actively launching new merchandise and augmenting capacities to strengthen model presence throughout India.

- Outpacing Business Development: Persistently outperformed trade progress over the previous 5 quarters.

- Enlargement into B2B: Latest entry into building chemical substances and putty segments diversifies the client base and marks a transition into the B2B market alongside conventional B2C.

- Community and Throughput Enchancment: Concentrate on increasing the seller community, enhancing throughput per lively seller, and growing tinting machine manufacturing exhibits promising progress potential.

Valuation

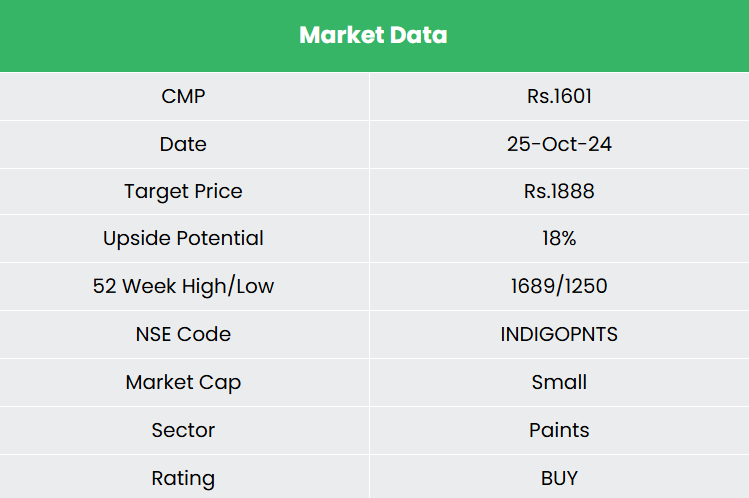

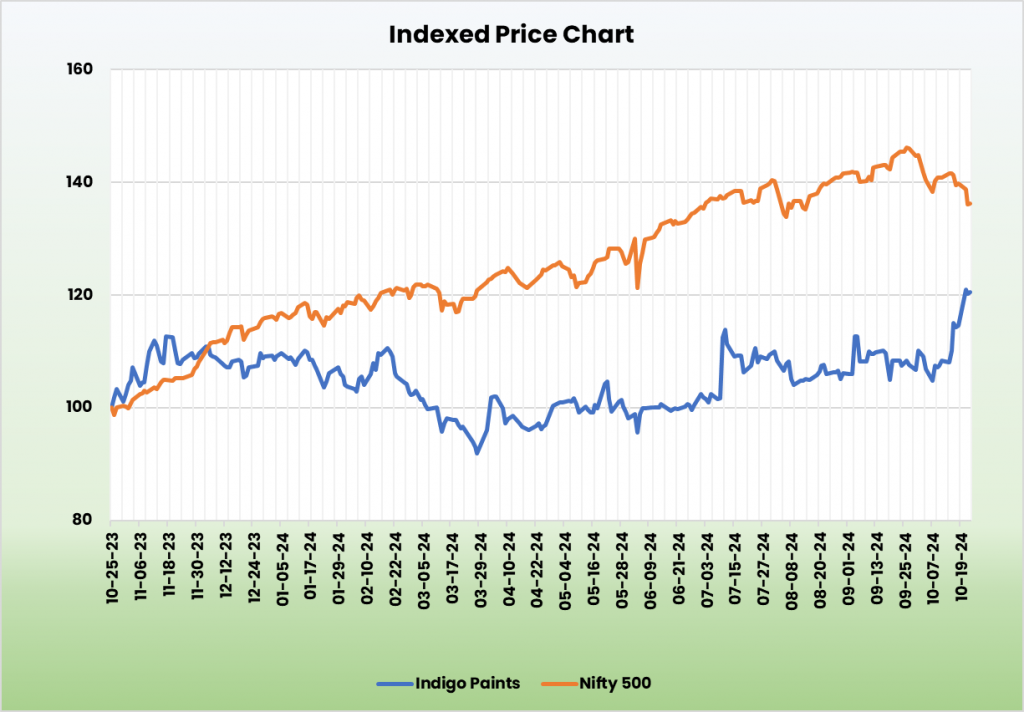

Indigo Paints’ technique of increasing into Tier 3 and 4 cities whereas steadily rising in Tier 1 and a pair of markets, alongside capturing market share from organized rivals and enhancing its waterproofing product choices, helps its robust efficiency. The corporate’s entry into venture gross sales and building chemical substances, mixed with elevated manufacturing capability, additional drives progress. We suggest a BUY score with a goal worth (TP) of ₹1,888, primarily based on a valuation of 55x FY26E EPS.

Dangers

- Aggressive Depth: Heightened competitors from current gamers and the entry of recent rivals could affect revenue margins.

- Uncooked Materials Worth Volatility: Fluctuations within the costs of key uncooked supplies like titanium dioxide and monomers, influenced by crude oil worth volatility, can adversely have an effect on margins.

Notice: Please observe that this isn’t a suggestion and is meant just for academic functions. So, kindly seek the advice of your monetary advisor earlier than investing.

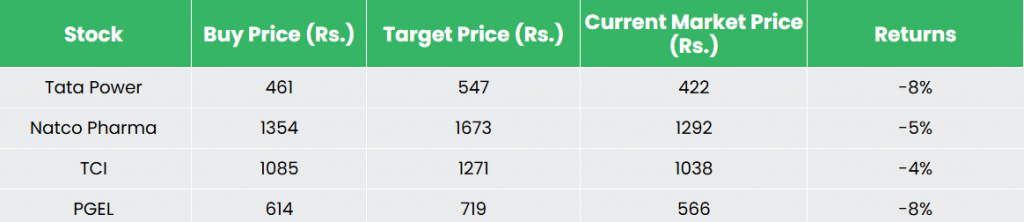

Recap of our earlier suggestions (As on 25 October 2024)

Tata Energy Firm Ltd

Natco Pharma Ltd

Transport Company of India Ltd

PG Electroplast Ltd

Different articles you could like

Submit Views:

61