Introduction

Established in 1935 and headquartered in Mumbai, Cipla Ltd. is a world pharmaceutical firm famend for its sturdy presence in key markets equivalent to India, South Africa, North America, and different regulated and rising areas. Cipla is devoted to offering high-quality, inexpensive drugs and has a various portfolio that features remedies for respiratory, cardiovascular, and infectious illnesses, amongst others. With a dedication to innovation and sustainability, Cipla continues to make vital strides in enhancing healthcare entry and outcomes worldwide.

Product Portfolio

– Generics and branded generics

– Over-the-counter (OTC) merchandise

– Specialty and client well being merchandise

– Respiratory medicine

– Anti-retroviral drugs

– Urology, cardiology, anti-infective, CNS, and different therapeutic segments

– 1500+ merchandise in 65 therapeutic classes accessible in over 50 dosage kinds

Subsidiaries as of FY23:

– 45 subsidiaries

– 8 affiliate firms

Development Methods of CIPLA

– Cipla has achieved gross sales exceeding $500 million previously 4 years, positioning it because the fastest-growing US generic pharmaceutical firm amongst its rivals.

– The corporate’s Indian operations have skilled sturdy development of 10% in FY24, pushed by elevated demand for branded prescription drugs and commerce generics.

-Cipla boosted its market share in North America by 15.5% in FY24, pushed by vital shares in key markets equivalent to Lanreotide and Albuterol.

-South Africa’s Non-public Market witnessed distinctive year-on-year development of 26% in native forex phrases, surpassing total market development charges.

-Strategic filings embrace 5 respiratory property, together with gSymbicort and gQvar, with launches anticipated throughout the subsequent three years.

-The corporate has filed 12 property in peptides and complicated generics, slated for launch over the following 2-4 years, illustrating a centered growth into specialised segments.

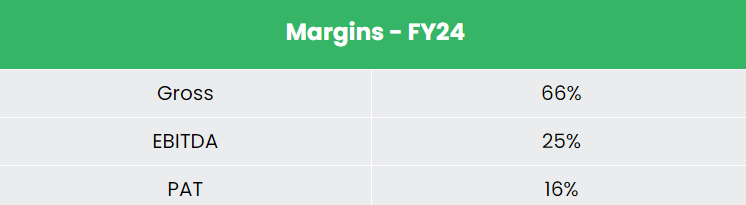

CIPLA Ltd Monetary Highlights

Q4FY24

– Income: Rs.6,163 crore (7% improve YoY)

– Working revenue: Rs.1,316 crore (12% improve YoY)

– Internet revenue: Rs.932 crore (79% improve YoY)

– Working revenue margin: 21% (54 bps YoY enchancment)

– Internet revenue margin: 15% (587 bps YoY enchancment)

– R&D expenditure: Rs.444 crore (19% YoY improve)

FY24

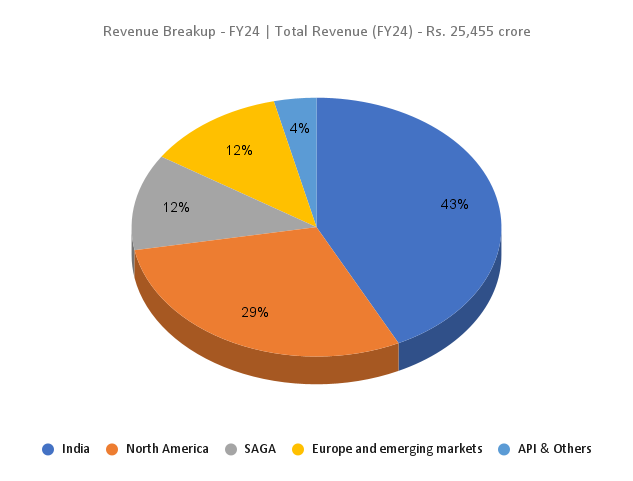

– Income: Rs.25,455 crore (14% improve YoY)

– Working revenue: Rs.6,233 crore (26% improve YoY)

– Internet revenue: Rs.4,106 crore (47% improve YoY)

Monetary Efficiency (FY19-24)

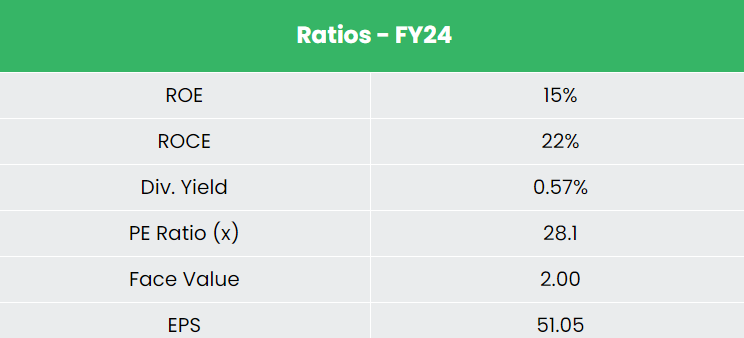

– Income and PAT CAGR: 10% and 25%

– Common 5-year ROE: 14%

– Common 5-year ROCE: 17%

– Debt-to-equity ratio: 0.02

Business Outlook

– India is the most important supplier of generic medicine globally

– Indian pharmaceutical trade: third largest by quantity, 14th largest by worth

– Projected CAGR of over 10% to succeed in US$ 130 billion by 2030 and US$ 450 billion by 2047

– Largest variety of USFDA-compliant pharmaceutical vegetation outdoors the US

– 2,000+ WHO-GMP accredited amenities serving demand from 150+ international locations

Development Drivers

– 100% FDI allowed by computerized route for Greenfield prescribed drugs initiatives

– Rs.1,000 crore (US$ 120 million) earmarked for promotion of bulk drug parks in FY25

– PLI scheme for prescribed drugs with a complete outlay of Rs. 15,000 crore (US$ 2.04 billion) from 2020-21 to 2028-29

Aggressive Benefit

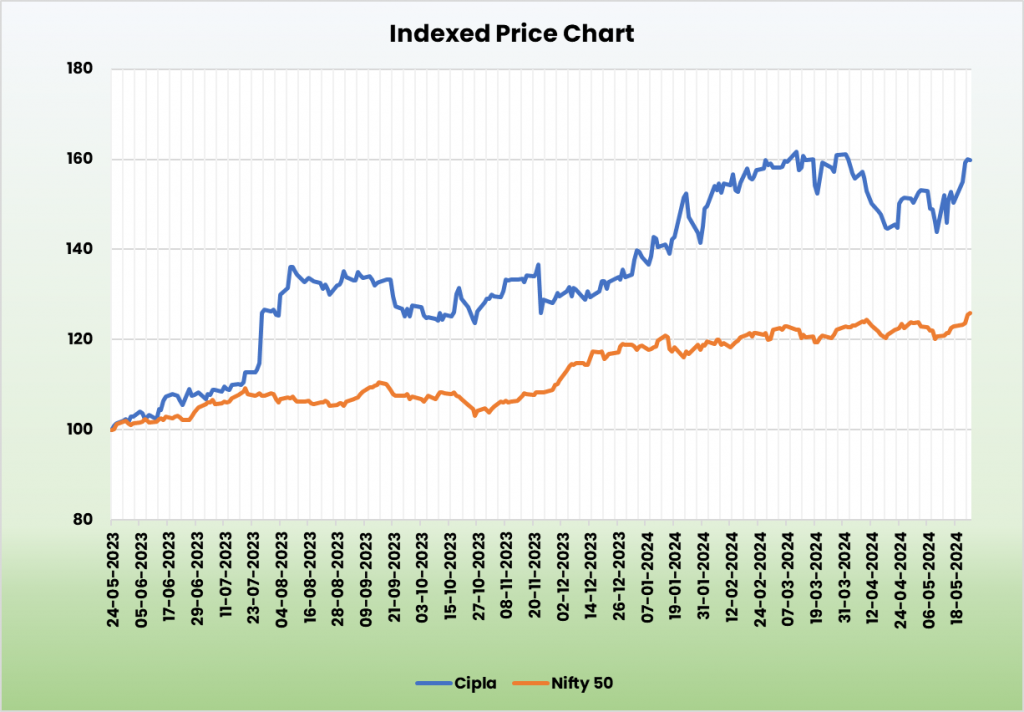

In comparison with rivals like Solar Prescribed drugs Industries Ltd and Lupin Ltd, Cipla stands out as an undervalued inventory with vital potential for P/E growth, supported by its sturdy margin and earnings development

Outlook

- Cipla Ltd. has been essential in making inexpensive HIV remedy accessible from India.

- Cipla is growing new merchandise together with inhaled insulin and plazomicin, with extra within the pipeline.

- The corporate goals to rank 2nd in OTC markets and launch peptide property in FY25.

- Cipla is growing advanced ANDA merchandise for its future portfolio.

- Cipla plans to speculate Rs.1,500 crore to boost manufacturing and sustainability, with an EBITDA steering of 24.5% to 25.5%.

Valuation

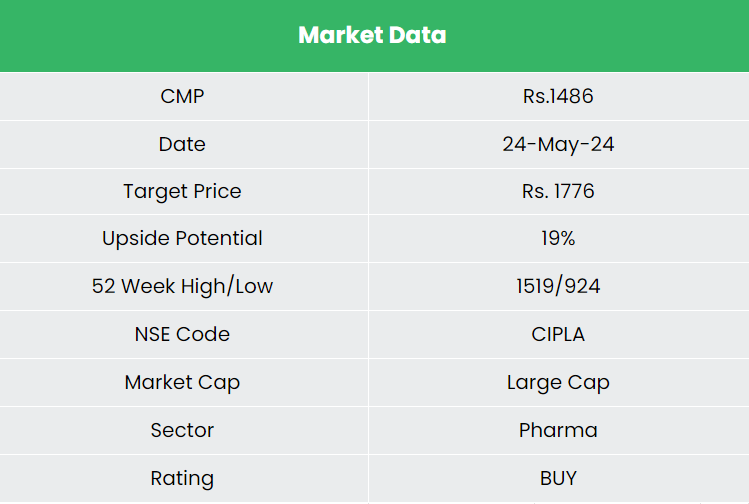

With an improved product combine, deepening distribution community, and technological improvements, Cipla is predicted to see appreciable development in income and margins. A BUY score is beneficial with a goal worth (TP) of Rs. 1,776, 32x FY26E EPS.

Dangers

– Foreign exchange danger resulting from vital operations in overseas markets.

– Regulatory danger, together with scrutiny by regulatory businesses just like the USFDA.

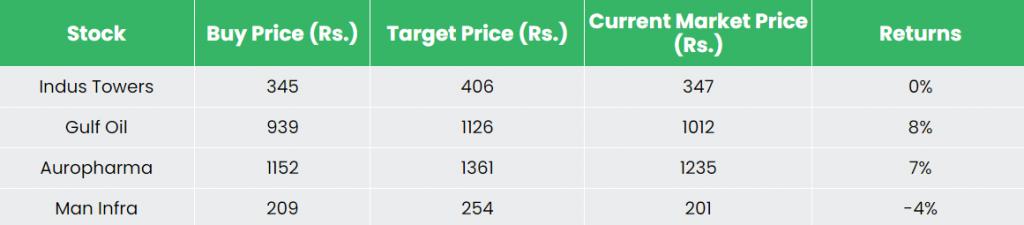

Recap of our earlier suggestions (As on 24 Might 2024)

Indus Towers Ltd

Gulf Oil Lubricants India Ltd

Aurobindo Pharma Ltd

Man Infraconstruction Ltd

Different articles you might like

Put up Views:

793